# Consumer Price Index DeFi Hedged | CPIDH

CPIDH - Consumer Price Index DeFi Hedged tracks aggregated changes in the consumer pricing index against returns in the crypto market. This is a direct correlation to cryptocurrency markets and their shifts between store of value and recognition as risk assets.

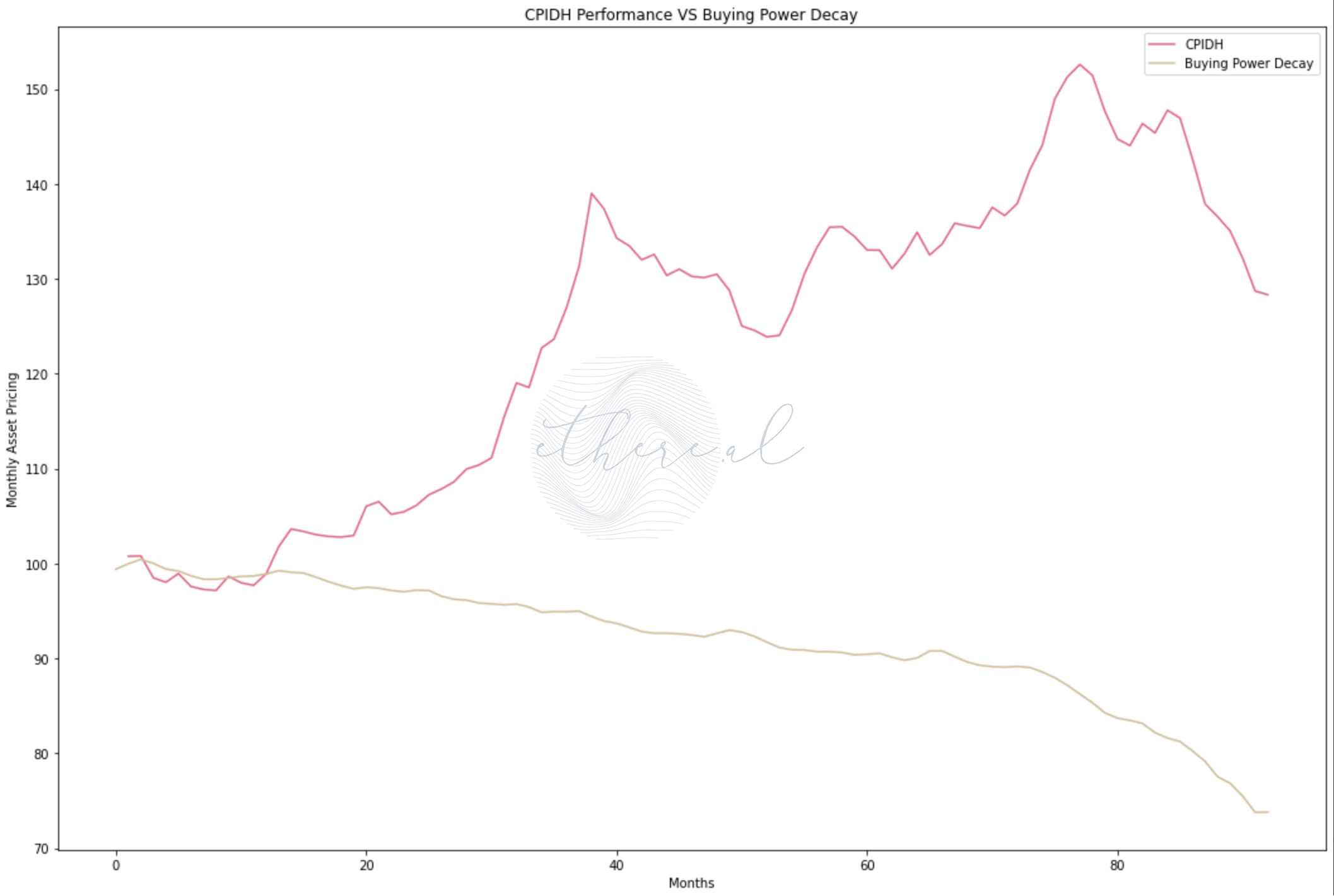

#### CPIDH performance VS Buying Power Reduction MoM. Click below to enlarge.

If the correlation between the two strengthen, resulting in cryptocurrency markets appreciating in value against the reads - this asset is structured to appreciate in value. The opposite is also true if cryptocurrency markets shift towards risk status. However, volatility is baked into the product, therefore it can have wider fluctuations based on said correlations as well as typical market swings. As such, it can act as a shorter to mid-term trading tool based on portfolio bias of the aforementioned.

Mints start at 10 USD worth of ISA and will theoretically trade as a summation of the aforementioned ratios. The higher the correlation, the more sensitive CPIDH is to positive moves. The lower the correlation, the less sensitive the asset trades. Over time - the range will rise or fall based on the relationship between the two, but the bias representation will remain consistent.

Like all collateralized products on our platform, sRho is used to secure the short position. CPIDH utilizes a 2:1 collateral ratio to secure the position. A 2.5% mint fee is required to mint CPIDH - with the minter receiving sCPIDH in return as a receipt.

A 2.5% fee applies to swapping sCPIDH. sCPIDH can be bonded and sold to the Treasury. Short-sellers will also pay interest to the pooled long sDGM at a daily interest rate of 0.2% per day - which will be paid for in sRHO. This daily interest will be calculated at the time of establishing the short by entering the maximum number of days you will be short for. Once the time limit is up - the short contract will expire and the short closed. If CPIDH is below the price when the short was initiated, the aggregated long pool of CPIDH will pay the unit count worth of profit to the now closed short holder. The time interest the short paid to the collected pool of longs will then be distributed to the longs proportional to their positional unit count.

However, the interest will only be paid to the long holders that were in the pool at the time the short was established. If a short-seller chooses to close out their position at a loss, the collateral lost will be divided among all long sCPIDH unit holders that were in the pool at the time the short was established. If the short-seller closes out their position at a profit, the percentage of the profit will be divided amongst all long-holders and the appropriate sCPIDH units will be transferred to the short-seller as profit.

**Shorting above the total float of CPIDH in the lending pool is prohibited.**